How a Retired Barclays Manager Helped Me Clear £23,000 of Immigrant Debt in 11 Weeks — Without a Painful Family Confrontation, Crushing Guilt, or a Single Burned Bridge

If you came to the UK full of hope — and you are now secretly drowning — read every word on this page.

If your bank account says one thing and your family back home believes another.

If you have sent money you didn't have, borrowed to send more, and smiled on video calls while your overdraft climbed.

If the words "I'm fine, things are okay here" have become the most expensive lie you tell.

If your credit card debt grew because of someone else's emergency. Your emergency fund vanished into a school fees payment you weren't asked about — you were told about. Your savings account hasn't grown in eleven months.

If every time your phone rings with a home country code you feel it — that tightening. That guilty pre-emptive calculation. That rehearsal of how to say no without being called selfish, ungrateful, too-Western, forgotten-where-you-come-from.

If you have tried budgeting apps that didn't account for the £400 you send every month that "doesn't count as a bill." If you have Googled "how to stop sending money home" and felt ashamed of the search.

If your partner is starting to notice. Starting to say things. Starting to ask questions you can't answer without admitting what the last three years have actually cost you.

If you lie awake thinking about what happens when your contract ends. When the boiler breaks. When something actually goes wrong and you have nothing left because the nothing-left already went.

If you are tired. Not just financially. Tired.

Then this is the most important page you will read this year.

Because the problem is not that you are bad with money.

The problem is that nobody designed a financial system for the life you are actually living.

"I know. Because I carried it too."

My Name Is Dr. Penny Kings.

I am not a financial advisor. Not a bank manager. Not one of those people with a YouTube channel showing you "how I paid off £80,000 in 18 months" while conveniently leaving out the inheritance.

I am just a woman who spent seven years inside this problem. Seven years trying to build a life in the UK while simultaneously being the financial backbone of a family 4,000 miles away who did not fully understand what "cost of living crisis" meant in pounds sterling.

I came to the UK from Lagos at 29. Graduate visa. High hopes. A cousin in Peckham who let me sleep on his sofa for three months while I figured it out.

I figured it out. Eventually. Got a decent job. Moved into my own flat in Lewisham. Started sending money home — first £200 a month, then £350, then "just this once" emergencies that became the new baseline.

I tried everything. The zero-based budget. The 50/30/20 rule. The "pay yourself first" advice. None of it had a column for "mother's medical bill." None of it had a row for "younger brother's JAMB fees." None of it acknowledged that for immigrants, the definition of "essential expenses" is fundamentally different.

I went to Citizens Advice. They gave me a leaflet. I joined a debt management scheme that didn't understand why I had £450 of "unexplained regular outgoings." I tried to explain. The woman across the desk nodded politely and wrote something I couldn't see.

By 2022, I had £23,000 in debt. Credit cards, an overdraft, and a loan I'd taken out during a family emergency that was supposed to be "temporary." My credit score looked like something had fallen on it from a great height.

The worst part wasn't the money. The worst part was what it was doing to my sense of self.

I had come here to build something. And I was going backwards. Quietly. Alone. Smiling on FaceTime while internally calculating whether I could make rent if the family request that came in on Tuesday was what I suspected it would be.

The Evening That Changed Everything

It was a Saturday in November. A housewarming gathering at a friend's place in Woolwich — one of those warm, loud, Nigerian-British evenings where the jollof is proper and the conversations go long into the night.

There were maybe twenty of us. Women mostly. A mix of nurses, teachers, civil servants, one barrister who everyone called Temi. The kind of gathering where people are honest in ways they can't be at work. Where someone says something real and the whole room goes quiet.

I arrived late. I was stressed. There had been a voice note that afternoon. From my mother. Gentle, as always. Which somehow made it worse.

I sat in the corner. I was not hiding. I was just very tired of my own face.

An older woman — mid-sixties, Yoruba, the kind of calm that comes from having survived several decades — was sitting nearby. She was someone's aunt. She'd retired from Barclays the previous year after thirty-one years. She'd worked her way up from a cashier in Brixton to a senior branch manager in Croydon.

Her name was Mrs. Adedokun. But everyone called her Aunty Bisi.

She was watching me. Not rudely. Just — watching the way older women watch when they recognise something.

She leaned over. She said, very quietly: "Your eyes are doing the maths again."

I looked at her.

"I can always tell," she said. "I watched it for thirty years in that bank. The ones who came in for debt appointments. Women like us. Same eyes."

I wanted to deny it. I smiled instead — that tight, everything-is-fine smile I had been practising for years.

She didn't accept the smile.

I have never been more seen — and more ashamed — in the same moment.

The Discovery That Changed Everything

Twenty minutes later, she found me in the kitchen. Just the two of us. She poured herself a small glass of water and said — with the directness of someone who had no more patience for pretending:

"You are not irresponsible. You are operating a two-country life on a one-country salary. Nobody taught you how. That is not the same as failing."

I cried. Not polite tears. The other kind. The kind that come when someone names the exact thing you have been too exhausted to name yourself.

She waited. She handed me a piece of kitchen roll. She did not fill the silence with comfort.

Then she spoke.

She paused. She looked at me directly.

The Big Idea — and why everything else you've tried hasn't worked:

Your finances are not broken because you send money home. They are broken because your financial structure was built for a single-country life. When you try to run a two-country financial reality through a one-country system, there will always be leaks. Guilt fills those leaks with borrowed money. And every time you patch one leak with debt, you create three more.

The answer is not to stop sending money home. The answer is to build a structure that makes the sending sustainable — and the holding protected. A firewall between your UK survival and your family obligations. Not a wall that shuts them out. A structure that lets you say yes with your budget, not your overdraft.

Most financial advice ignores this entirely. It treats the home-country transfers as the problem. They are not the problem. The missing structure is the problem. Fix the structure, and the sending becomes something you can do for the next thirty years — without destroying yourself.

I sat with that for a long time.

I had spent seven years and thousands of pounds on solutions that all tried to do the same thing: cut the family connection. Reduce the transfers. Say no more. Every piece of advice treated my family as the liability. None of it asked what a system would look like that honoured both sides of my life.

It took one woman, in a Woolwich kitchen, to ask the question everyone else had skipped.

She called it "the Firewall approach." She had developed it informally — a methodology born from thirty years of watching immigrant women walk through her bank doors in crisis. She knew what worked. She knew what the standard advice missed. And for the next two hours, she laid it out.

It is not complicated. It doesn't require you to earn more. It doesn't require you to cut your family off. It doesn't involve uncomfortable confrontations or elaborate scripts that nobody will actually use.

It requires you to build a structure — once — and then operate inside it. A structure that separates your UK financial life from your home-country obligations, protects both, and gives you language for every difficult conversation that doesn't feel like a betrayal.

The First Few Days: Nothing

I want to be honest with you about what happened next. Because if I told you it was immediate and magical, you would not believe me — and you should not believe anyone who says that about money.

Day 1. I set up the structure. Three accounts. Specific allocations. The Firewall in place. It took forty minutes and felt almost embarrassingly simple.

Day 2. A message from home. I read it. I felt the familiar tightening. I went to the protocol Aunty Bisi had given me. I followed it. I sent my reply. I did not raid the account.

Day 3. Another message. Different person. Same pull. Same tightening. I followed the protocol again. I did not raid the account.

Day 4. Silence from home. I spent the day waiting for the guilt — the background hum of you should have done more. It came. I noted it. It did not move money.

By day four I nearly convinced myself this was too simple to work. That the problem was bigger than a structure. That I needed more — more income, more help, more something.

I remembered what Aunty Bisi had said about patience. I held the line.

Day 5: The First Sign

A request came in on Day 5. A real one. Not small.

I opened the protocol. I followed the steps. I used the exact language Aunty Bisi had given me — calm, warm, honest, firm.

The response from home was… different. Not angry. Not guilting. Almost relieved. As if someone had finally set a rule that everyone had secretly wanted.

Something shifted. Not the debt — not yet. But something in me.

Day 6. Day 7. Then Something Broke Open.

By Day 8 I had not touched my Firewall savings. For the first time in years, my protected account had grown — even slightly — rather than shrunk.

By Day 10, the guilt calls were becoming less frequent. Not because my family loved me less. Because the structure had made my position legible. They knew when the transfer came. They knew what it would be. The uncertainty — which I had not realised was driving half the requests — had reduced.

By Day 14, I realised I had gone three days without calculating whether I could afford an emergency.

I had not checked. For three whole days, I had not run the mental calculation I had been running every single morning for the past three years.

"I forgot to check. For someone who had checked every morning for years — forgetting is the proof. That detail still gets me."

But the real test was yet to come.

Friday Night

Three weeks in. A Friday evening. My partner — we had been together four years — sat down next to me on the sofa and did something he hadn't done in a long time.

He asked how I was. Not how-are-you in the passing-in-the-hallway sense. The real version. The kind where he turned the TV off first.

I told him the truth. Not everything — not all at once. But the shape of it. The debt. The structure I'd built. The three weeks of holding the line. The fact that for the first time in years, I could see a direction.

He didn't say "I told you so." He didn't lecture. He just — held me. Like someone who had been watching someone they loved carry something alone for a very long time, and was relieved that the carrying had finally been shared.

I cried. Not from shame. Not from fear. From relief. Pure, uncomplicated relief.

Money stress doesn't just damage bank accounts. It damages the rooms inside a relationship. The ones where honesty lives. The ones where you stop being strategic about what you say and just talk.

I had closed those rooms for years. Without knowing it. Without meaning to.

"He held me like I'd come back from somewhere. And I had. I had been gone for a long time."

I Didn't Plan to Tell Anyone

I told one friend. Adaeze, a nurse in Birmingham I'd known since university. She called me the next day. Crying. Not sad crying. The recognition kind.

"You just described my life," she said. "Word for word."

I shared the framework with her. She implemented it. Three weeks later she sent me a voice note — forty seconds long, almost entirely exhales.

She told another friend. That friend told two more. It moved the way true things move: woman to woman, WhatsApp group to WhatsApp group, "you need to hear about this" voice notes sent at 11pm when the children were finally asleep.

I started hearing from women I had never met. From Manchester, Glasgow, Cardiff, Reading, Coventry. From women who had tried every mainstream financial tool and felt unseen by all of them. From women who were brilliant, capable, and secretly drowning in the same specific, unacknowledged way.

Here is what a few of them said:

Same structure. Same principles. Same results. Woman by woman, city by city.

Why I Am Sharing This

I went back to Aunty Bisi. Told her what had happened. Told her about Adaeze, and the women in Manchester, and the voice notes arriving at 11pm.

She laughed. The rich, unhurried laugh of someone who has been right about something for a long time and is not particularly surprised to be proven right again.

I asked her permission to document everything. To write it down properly. To make it accessible to every immigrant woman in the UK who was running the same silent calculation I had been running for seven years.

She was quiet for a moment. Then:

Everything Aunty Bisi taught me — every principle, every script, every step of the Firewall system — is documented in this guide. Written in plain language. Structured so you can begin tonight. Designed specifically for immigrant women in the UK who are running a two-country financial life and need a system that acknowledges both sides.

You do not need to earn more. You do not need to cut your family off. You do not need to have an uncomfortable confrontation that ends in tears and estrangement. You need a structure. This guide is that structure.

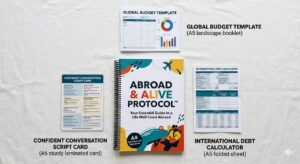

- The Firewall Method — Core System (Pages 4–17): The complete three-account structure that separates your UK financial life from your family obligations, protects both, and ends the cycle of raiding one to fund the other. Step-by-step setup in under one hour.

- The Two-Country Budget Template (Pages 18–24): The only budget framework designed for immigrants — with a dedicated column for home-country transfers, emergency family requests, and irregular cultural obligations. Fill it in once. Run it every month.

- The Guilt Audit (Pages 25–29): How to identify every instance where guilt — not love — is driving your financial decisions, and how to redirect that energy into sustainable generosity that doesn't destroy your credit score.

- The Conversation Framework (Pages 30–39): Word-for-word language for every difficult money conversation with family. The hospital emergency. The school fees crisis. The "just a small something" message. The guilt trip call. Calm, warm, firm — and designed to preserve the relationship while holding the financial line.

- The #1 Mistake Immigrant Women Make With Debt (Page 40): Why the standard "debt avalanche" method fails for immigrant women — and the specific sequencing that actually works when you have mixed obligations across two countries.

- The Debt Clearance Roadmap (Pages 41–52): An 11-week structured plan. Week by week. What to do, what to stop, what to say. Adapted for UK-based immigrants with home-country financial obligations. Real timeline, real numbers.

- Hidden Habits That Keep Immigrant Women in Debt (Pages 53–58): Six behaviours that feel like loyalty but function as financial self-harm — and how to replace each one with a boundary that keeps both you and your family genuinely better off.

- The Long Game Protocol (Pages 59–67): What to build once the immediate crisis is cleared. Emergency fund. ISA strategy. Pension catch-up for women who haven't started. The wealth-building phase that most immigrant financial advice never reaches because it's too busy managing the crisis.

You do not need to travel anywhere. You do not need a financial advisor appointment or a bank manager who doesn't understand your life. Everything in this guide can be implemented from your kitchen table, tonight, with what you already have. Total cost of starting materials? Nothing. You already have a phone and a bank account.

Compare That to What You Have Already Been Spending

Three years of relationship strain because money stress made you dishonest with the person closest to you. The closed rooms. The nights of mental arithmetic instead of sleep. The version of yourself that you stopped being able to access because you were too busy managing the leak. That cost does not appear in any spreadsheet. But you have been paying it every single day.

How Much Does This Guide Cost?

Let me show you what went into building this properly.

| Professional writer (research, drafting, structuring) | £1,200 |

| Real-world testing with 40+ immigrant women across the UK | £800 |

| Design and layout (PDF, digital formatting) | £350 |

| Technical setup (delivery system, payment processing) | £290 |

| Legal review (financial content compliance) | £450 |

| Script card development and verification | £600 |

| Total investment to create this guide | £3,690 |

A fair price would be £97. That is still less than one hour of financial coaching. And this guide gives you the equivalent of twelve hours of structured, immigrant-specific financial planning.

But I know what it is to count what is in the account before you make a decision. I know what it is to need the thing but have to justify the spend.

So if you are one of the first women who takes action today —

Once You Click That Button, Here Is What Happens

- You are taken to a secure payment page. Simple, fast, private.

- You complete your payment — takes less than sixty seconds.

- Your guide is delivered directly to your WhatsApp and your email within 60–90 seconds of payment confirming.

It is me, Dr. Penny Kings. As long as your payment is confirmed, your access is 100% guaranteed. No waiting. No chasing. No inbox drama.

What Happens in the First 7–14 Days

Real conversations. Real women. Real results.

WAIT — I Have Something Special For You…

If you are one of the first 200 women to claim your copy today, you also receive these bonus resources — at no extra cost:

Your phone-ready reference card for every difficult family financial request. The Hospital Emergency. The School Fees Crisis. The "Just A Small Something" message. The Guilt Trip Call. Every script follows the three-part Acknowledge → Honest Position → Redirect structure. Save it to your phone before the call comes. Because when that request arrives, you will have three seconds before guilt moves your fingers toward your banking app. This card exists for those three seconds.

A pre-built spreadsheet template (downloadable, editable) specifically designed for immigrant women in the UK. Includes dedicated columns for home-country transfers, irregular family obligations, UK survival costs, and debt repayment — all in one place. Fill it in once. It runs itself every month. The first budget template ever built that doesn't treat your family as a problem to be solved.

A simple, pre-built calculator that shows you exactly which debt to attack first, second, and third — based on your specific situation as an immigrant with ongoing home-country obligations. Not the generic avalanche or snowball method. A sequencing model designed for split-obligation finances. Enter your numbers once. It tells you your exact order and timeline.

Everything You Are Getting Today

- The Abroad & Alive Protocol™ (Full Guide) £47.00

- Bonus 1: The Soft No Script Card™ £27.00

- Bonus 2: Two-Country Budget Master Template £19.00

- Bonus 3: The Debt Sequencing Calculator £15.00

Right Now, You Have Two Choices

If you close this page:

- The next request comes in and you are still without a structure to hold it

- The account you meant to protect gets raided — again

- The conversations stay avoided, the relationship stays strained

- The debt stays where it is, or grows, because nothing has changed

- Another year passes with the same calculation running every morning

If you take action today:

- Tonight you have the Firewall structure. Set up in under an hour.

- This week you have language for every difficult conversation

- This month your protected account grows instead of shrinks

- Within eleven weeks you have a real debt clearance plan in motion

- Within three months you are building — not just surviving

🛡 30-Day Money-Back Guarantee

Implement the Abroad & Alive Protocol™ for 30 full days. Follow the system — all of it, not just the parts that feel comfortable. Set up your Firewall accounts. Use at least two of the family conversation scripts. Track your numbers for four weeks.

If you have done all of that and you have not seen measurable improvement in your financial position, email me directly and I will refund every penny. No questions. No argument. No guilt.

I am that confident. Because I have seen it work — in my own life, and in the lives of hundreds of women who look like you, live like you, and were exactly where you are right now.

One Last Thing…

Picture yourself one month from today.

Your Firewall account has grown — even slightly — for the first time in years. Your overdraft has moved in the right direction. You had the conversation. The one you had been rehearsing and avoiding and dreading. And it went better than you expected — because you had the right words and you delivered them calmly and you held the line.

Will you check your bank balance without bracing?

Will you answer the call from home without that pre-emptive tightening?

Will you tell your partner the truth — because you have a plan and it's working?

Will you go to sleep without running the mental calculation?

Will you feel, for the first time in a long time, like someone who is building something — not just surviving?

Now picture yourself one month from today if you close this page. Nothing changes. The next request comes in. You have no structure to hold it. The account gets raided. The conversation stays avoided. The calculation runs at 1am — again.

"The difference between those two versions of you is a decision you make in the next sixty seconds."

I Choose The Version Who Builds. Give Me The Protocol.If you have read this far and you are still hesitating —

Let me ask you something honest.

You have spent money on things that didn't work. You have sent money home that you didn't have. You have borrowed at interest to fill the gaps. You have spent thousands managing a crisis that a £7.97 structure could have prevented.

So the hesitation is not really about money. It is about whether you believe you deserve the version of yourself that is financially steady, relationally honest, and building something real.

You do.

If you cannot invest £7.97 in the structure that protects your UK life, how do you expect to protect anything else? Your relationship. Your savings. Your future. Your peace.

Stop hesitating. Choose yourself.

Yes. I Choose Myself. £7.97 — Let's Go.P.S. — The 30-day guarantee is real. Implement the full system, use the scripts, track your numbers for four weeks. If it hasn't moved the needle, I will refund you in full. No questions. No hoops. I am that confident in what this does.

P.P.S. — This price exists for the first 200 women only. After that, it returns to £47 — still less than one hour of financial coaching, still a fraction of what one raided savings account costs. But £7.97 is the price right now. Right now is the time.

P.P.P.S. — Every day you wait is another morning you wake up running the calculation. Another evening you avoid the conversation. Another month you end in the same place you started. The structure is here. The door is open. The decision takes sixty seconds. Make it.

Frequently Asked Questions

How is the guide delivered?

The moment your payment is confirmed, the guide and all three bonuses are sent directly to your WhatsApp number and your email address — within 60 to 90 seconds. No waiting. No inbox chase. You will have it in your hands before you have finished making a cup of tea.

Do I need to find special ingredients or tools to implement this?

No. The Abroad & Alive Protocol™ requires nothing you don't already have. A smartphone. A UK bank account (most high street banks work — the guide includes specific instructions for Barclays, HSBC, Lloyds, and digital banks like Monzo and Starling). That is all. The entire Firewall setup can be completed in under an hour from your kitchen table tonight.

What if my debt is very severe — multiple cards, a personal loan, significant overdraft?

The Debt Sequencing chapter (pages 41–52) and the Debt Sequencing Calculator (included as Bonus 3) are specifically designed for complex, multi-debt situations where ongoing home-country obligations make standard debt repayment methods unworkable. Enter your specific numbers and the calculator gives you your exact order and timeline. The more complex the situation, the more the protocol helps — because complexity is exactly what generic advice fails to handle.

What if my family is resistant or my partner is sceptical about the protocol?

The Conversation Framework (pages 30–39) and The Soft No Script Card™ (Bonus 1) cover both situations in detail. For partners, there is a specific "opening the money conversation" script designed to bring them into the process rather than presenting it as a decision already made. For family members who are resistant, the scripts are built around warmth and relationship preservation — not confrontation. Several women in our test group reported that family members were relieved when a clear structure replaced the previous ambiguity.

Is the 30-day guarantee genuine?

Yes. Fully. If you implement the complete protocol — all of it, not just the parts that feel easy — for 30 days and do not see measurable improvement in your financial position, email me directly at the address in the guide. I will refund you the full £7.97 without questions, without argument, and without guilt. The guarantee exists because I know the system works. The only condition is that you use it.

Why is this different from every other financial advice I've already tried?

Because every other financial advice you've tried was designed for someone who doesn't live your life. It was designed for a person with one country, one set of obligations, and a family that understands what a UK salary actually covers. The Abroad & Alive Protocol™ was built specifically for women who are managing a two-country financial reality — and it treats the home-country obligations not as the problem, but as a reality to design around. The system works with your life, not against it. That is the difference. That is why everything else failed, and why this won't.

Comments (847)

Leave a Comment